Reporting Highlights

- Misplaced Investments: Individuals who invested with a Dallas HomeVestors franchise, as soon as touted as the biggest, accuse the proprietor of working a scheme that price them tens of tens of millions of {dollars}.

- Pink Flags: HomeVestors says its franchises observe greatest enterprise practices. However buyers say lax oversight allowed the “We Purchase Ugly Homes” model for use to additional the scheme.

- Firm Responds: HomeVestors has denied accountability for the franchisee’s actions, saying its franchises are independently operated. It has sued the franchise proprietor.

These highlights have been written by the reporters and editors who labored on this story.

Ronald Carver was skeptical when his funding adviser first tried to promote him on an “ugly homes” funding alternative eight years in the past. However as soon as the Texas retiree heard the small print, it appeared like a no-lose state of affairs.

Carver would lend cash to Charles Provider, proprietor of Dallas-based C&C Residential Properties, a high-producing franchise within the HomeVestors of America house-flipping chain identified for its ubiquitous “We Purchase Ugly Homes” ads. The enterprise would then use the {dollars} to buy properties wherein Carver would obtain an possession stake securing his funding and an annual return of 9%, paid in month-to-month installments.

“Worst case, I’d find yourself with a property price greater than what the mortgage was,” Carver mentioned of the pitch.

Carver began with a $115,000 mortgage in 2017. And certain sufficient, the curiosity funds arrived every month.

He had labored three a long time at a nuclear energy plant, and retired and not using a pension and earlier than he might acquire Social Safety. He and his spouse lived off the funding earnings.

The deal appeared so good, Carver talked his aged father into investing, beginning with $50,000. Because the month-to-month checks arrived as promised, each males elevated their investments. By 2024, Carver estimates they’d about $700,000 invested with Provider.

Then, final fall, the checks stopped. The cash Carver and his father had invested was gone.

Provider is accused of orchestrating a yearslong Ponzi scheme, bilking tens of tens of millions of {dollars} from scores of buyers, in line with a number of lawsuits and interviews with individuals who mentioned they misplaced cash. The monetary wreckage is strewn throughout Texas, having swept up each rich buyers and older folks with modest incomes who dug into retirement financial savings on the recommendation of the identical funding advisor utilized by Carver.

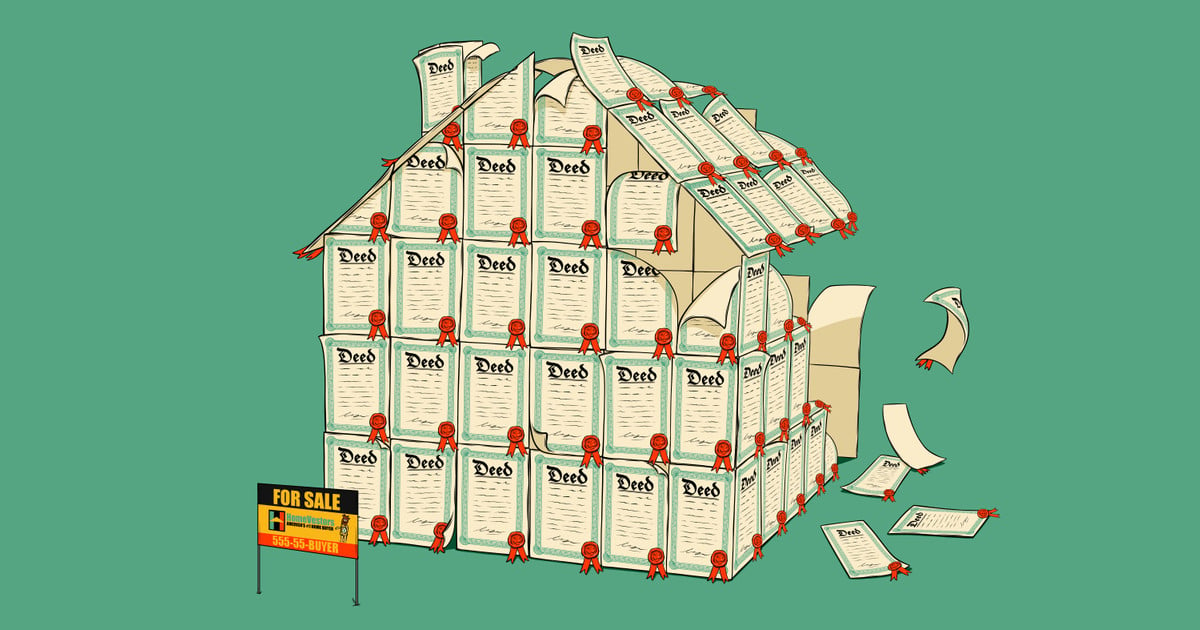

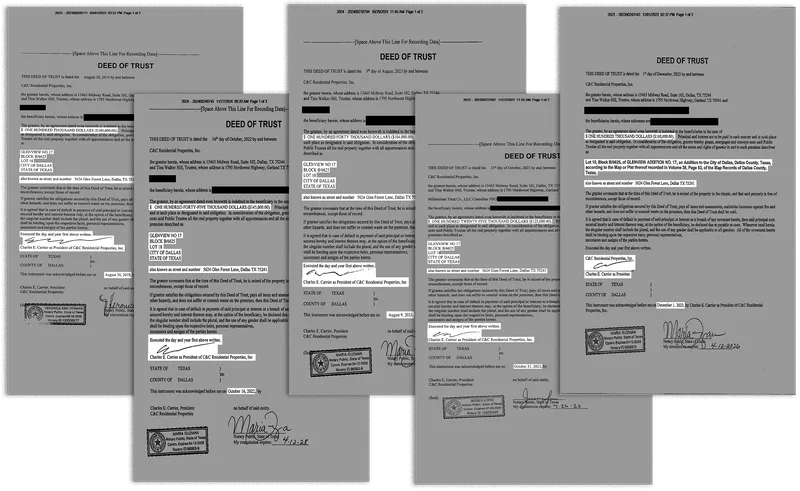

As early as 2020, Provider had begun taking out a number of loans on particular person properties — a few of which he by no means owned. In instances reviewed by ProPublica, as many as 5 notes have been recorded towards a single property, far exceeding the property’s worth. Provider additionally did not correctly file many deeds that have been alleged to safe the loans, accumulating extra debt than he might ever repay whereas buyers remained unaware they’d no collateral for his or her investments.

“It’s incalculable the quantity of harm this man did,” mentioned one investor who misplaced about $1 million and requested to not be named to keep away from embarrassment and to not intrude with a felony investigation into Provider’s scheme. “He’s ruined some lives.”

Provider, who declined an interview request, mentioned in a short cellphone dialog that he’s not making an attempt to keep away from accountability for the hurt he induced. “When this factor lastly stopped, it was utterly pushed by me saying ‘sufficient’ and going to the folks and saying, ‘Right here’s the mess I’ve created,’” he mentioned. “It is a mess created by me.”

Traders additionally blame HomeVestors. For practically 20 years, Provider used the corporate’s rigorously cultivated model because the “largest homebuyer in the USA” to achieve buyers’ belief. They accuse HomeVestors of failing to offer oversight that might have prevented the fraud, regardless of claiming to carry its franchises accountable for greatest enterprise practices. In its solutions to their lawsuits, HomeVestors has denied accountability for Provider’s actions, claiming its franchises are independently operated, regardless of incomes a whole bunch of hundreds of {dollars} from Provider’s enterprise.

HomeVestors revoked Provider’s franchise on Oct. 24, in regards to the time curiosity funds stopped arriving in buyers’ accounts. The corporate mentioned it had obtained a tip on its ethics hotline — created in 2023, after ProPublica detailed predatory shopping for practices by a number of franchises. When confronted by HomeVestors, Provider admitted that “he and his enterprise had entered into money owed that they may not pay,” a HomeVestors spokesperson mentioned. The corporate reported him to the FBI. In Might, HomeVestors filed swimsuit towards Provider for trademark infringement and for not indemnifying it towards these lawsuits.

“We take all allegations of misconduct extremely significantly as demonstrated by our decisive motion,” the spokesperson mentioned. “It’s actually disheartening for us that anybody who lent Mr. Provider cash was misled or harmed by his alleged fraudulent exercise.”

Now, Provider is underneath investigation by the Division of Justice, in line with a recording of an April name between the lead prosecutor and potential victims. (The FBI and DOJ declined to remark.) A choose in one of many many lawsuits towards Provider has deemed allegations of fraudulent loans to be true as a result of Provider by no means answered the grievance. And the buyers are in a race with each other to recoup even a small quantity of what they misplaced, by both ready for the DOJ to pay restitution, suing Provider or making an attempt to foreclose on properties nonetheless left in his portfolio.

Simply months after studying they’d misplaced all of their investments, and earlier than any restitution may very well be paid, Carver’s father died.

Credit score:

Obtained, collaged and highlighted by ProPublica

A Prime-Performing Franchise

In 2005, Provider opened a HomeVestors franchise in Dallas, the place HomeVestors is headquartered. Within the early days, information present, he relied on a handful of institutional lenders to finance his home purchases. Quickly, the Wharton Faculty of Enterprise MBA who had come to house-flipping following a profession at Pepsi and a meals service tools firm, began cultivating his rich mates for loans.

Provider didn’t match any stereotype of a glad-handing huckster with a nasty mortgage to promote. Those that knew him describe him as a critical particular person, “cordial however very direct.” He at all times had information in entrance of him, always specializing in his enterprise. It made him appear reliable, one investor mentioned.

At HomeVestors, he was held up as a mannequin franchise operator. C&C Residential Properties routinely made the highest quantity and high nearer lists and was even named franchise of the yr. Provider led coaching classes at firm conferences and described his enterprise as “the biggest and most profitable HomeVestors franchise in the USA” — a declare that remained on the web site for Provider’s enterprise via early Might.

“Chas Provider, for possibly 15 years, was one of many golden boys at HomeVestors,” mentioned Ben Ahern, who over 20 years labored for a HomeVestors franchise and later owned one earlier than leaving the corporate in 2021. “Internally, it was like, ‘Do no matter Chas Provider’s doing.’”

It isn’t uncommon for HomeVestors franchises to depend on personal buyers to finance their house-flipping. Banks aren’t sometimes concerned about house-flipping loans, which are sometimes short-term and riskier than a normal mortgage. Due to that threat, buyers who lend to house-flippers earn a considerably larger return.

To additional decrease their threat and guarantee they’d a official possession stake in the home, savvy buyers would confirm the transaction with an impartial title firm to analysis whether or not there have been different liens towards the property after which file the deed with the county recorder. However lots of Provider’s buyers, after years of constant funds led them to belief him, let Provider deal with recording the deeds and didn’t verify that he’d performed so.

As Provider grew his enterprise, he started relying extra on particular person buyers. ProPublica recognized via public information not less than 124 individuals who have lent cash to Provider since 2009. Not all of them have misplaced cash.

Provider’s seek for new buyers was aided by Robert Welborn, an funding adviser in Granbury, Texas, southwest of Dallas. Welborn had constructed a community of shoppers in Granbury, a metropolis of about 12,000 folks on the Brazos River, via church, friendships and referrals. A lot of his shoppers have been older and had modest nest eggs, which Welborn mentioned have been “effectively diversified.” He mentioned he constructed a relationship with Provider in 2012, after researching his background for about two months. That Provider was a profitable franchisee lent him credibility, Welborn mentioned.

“I by no means imagined the No. 1 franchisee with a fast-growing franchise firm, HomeVestors,” would defraud buyers, he mentioned.

On the time, Welborn additionally solicited new buyers with invites to steak dinners the place they might hear his pitch. An funding in Provider’s enterprise, in line with Welborn’s gross sales materials, which additionally featured the HomeVestors caveman mascot, Ug, was each profitable and safe. “Your funding is protected,” the gross sales materials assured potential shoppers.

For loans he despatched Provider’s approach, Welborn earned a 2% fee, he mentioned. Welborn had not less than two dozen shoppers who invested with Provider, most of whom had a number of loans to him, in line with a public information search. He wouldn’t touch upon what number of of his shoppers invested with Provider.

Many buyers have been pleased for years — in some instances, greater than a decade. The curiosity funds got here in like clockwork. Loads of Welborns’ shoppers relied on the funds for retirement earnings.

“I used to be actual tickled with it,” mentioned Tom Partitions, 85, who mentioned he misplaced $50,000 of his retirement financial savings by investing with Provider.

Some buyers observed small issues — a cost that arrived just a few days late or an error on the paperwork to safe the mortgage. However Provider at all times fastened the issues promptly, buyers mentioned.

“When you might have this 10-year steady, nice and mutually useful relationship, you construct up an excessive amount of belief,” mentioned John Moses, who estimates he misplaced greater than $1 million to Provider.

Trying again, the buyers who spoke with ProPublica mentioned they wished they’d taken these warning indicators extra significantly.

Credit score:

Max Erwin for ProPublica

“He Simply Pencil Whipped These Deeds”

By fall 2024, Provider’s funds to his lenders stopped. That’s when the home of playing cards fell.

Provider had spent that summer season scrambling for cash. Not solely did Provider should make mortgage funds to scores of buyers, however he additionally wanted to maintain up with the HomeVestors franchise charges and promoting funds. The corporate requires its franchises to make common reviews on gross sales and to open their books for audits, to offer monetary statements when requested, and to report all belongings and liabilities. Any of these reviews might have known as into query Provider’s means to remain solvent. However, in line with former franchise homeowners and workers, HomeVestors’ audits of its franchises are largely geared towards making certain they’re paying all their franchise charges, that are primarily based on gross sales.

Earlier than Provider’s tangle of fraudulent loans collapsed and was uncovered in court docket, there have been indicators of hassle.

In 2016, Provider was fined by the Texas Actual Property Fee for managing properties and not using a license. The HomeVestors franchise settlement requires homeowners to observe all legal guidelines and rules, notably actual property rules. In 2020, two title insurance coverage corporations issued particular alerts on Provider’s enterprise, advising their title officers to not enter into transactions with him with out additional authorized and underwriting assessment. Provider hasn’t paid taxes on a few of his properties since early 2023, in line with court docket and public information, one other violation of his franchise settlement. Regardless of the obvious violations, HomeVestors didn’t terminate Provider’s franchise settlement.

“I don’t actually suppose they do have a lot in place to forestall one thing like this,” Ahern, the previous HomeVestors franchise proprietor, mentioned of the corporate. “HomeVestors on the time didn’t appear to have an inner system policing how franchises finance shopping for properties.”

A HomeVestors spokesperson mentioned the corporate focuses on its franchise prospects’ experiences promoting their houses and doesn’t “dictate” how franchises elevate capital. “The greater than 950 franchises of HomeVestors are impartial companies with all kinds of finance choices accessible to them,” the spokesperson mentioned.

Final spring, Provider started borrowing towards his future receipts in alternate for money advances with exorbitant charges and annualized rates of interest that he later claimed ranged as excessive as 600%. Between Might and October, he did this not less than seven occasions, racking up greater than $1.2 million in debt past what he owed his buyers, displays included with court docket filings present. By fall, he owed greater than $75,000 in funds every week, in line with the unique phrases. Seven corporations filed swimsuit over the cash-advance agreements, accusing him of default. Provider has denied the allegations of default and has countersued 4 of the businesses, claiming he was charged unreasonably excessive rates of interest.

The lending scheme seems to have fallen in a grey space for state and federal securities rules. It’s unclear whether or not the promissory notes Provider issued to buyers meet the definition of a safety, two specialists advised ProPublica.

In October, Provider’s buyers started to confront him in regards to the lacking funds, together with Jeff Daly and Steve Needham, two of Provider’s largest buyers who had been lending him cash for years. Provider got here clear to Daly, admitting he had been operating a lending scheme for “a number of” years, in line with a lawsuit Daly and Needham filed. He advised Needham he had taken out a number of loans on particular person properties with out disclosing them to the buyers, in line with the lawsuit. The 2 males claimed of their lawsuit, which resulted in default judgments towards Provider, that mixed they’d misplaced $13.5 million to Provider.

The investor who spoke to ProPublica and requested to not be named mentioned in an interview that Provider broke down in tears when confronted about shedding greater than $1 million of the investor’s cash. Provider admitted the loans paid for his working bills, not for getting and refurbishing homes, the investor mentioned.

“He simply pencil whipped these deeds on the finish,” the investor mentioned, explaining that Provider drew up paperwork however didn’t file them. As a result of the deeds have been by no means recorded, the investor had no lien on the properties and due to this fact no collateral. Some deeds have been for homes that Provider didn’t personal or by no means purchased, the investor mentioned. “It was an entire fabrication.”

Welborn’s shoppers, who sometimes invested a lot smaller quantities with Provider, additionally realized of the house-flipper’s collapse within the fall, when their funds stopped. Carver mentioned that Welborn known as him a few days after the October cost was due and mentioned, “Hey, I’m sorry to let you know this, however Chas has known as me and admitted to fraud.”

Carver mentioned he received within the automobile and drove to Welborn’s workplace, the place he realized the nightmarish reality that each one the cash Provider had taken was gone.

“A Life-Altering Hit”

Traders are deploying quite a lot of methods to get their a refund — a few of which pit greater buyers towards smaller ones and early buyers towards newer ones. Those that acted rapidly are recovering some cash via foreclosures and lawsuit settlements. Though Provider is denying allegations in lawsuits introduced by the cash-advance corporations, he’s not preventing particular person buyers who’re suing him. Three of their lawsuits have resulted in judgments towards Provider, and he has up to now not defended himself towards the others.

Welborn mentioned he’s doing his greatest to assist his shoppers get better their cash by offering the mandatory paperwork, connecting them with consumers for the homes used as collateral and researching lien histories on the houses. When he first realized of the scheme, Welborn tried to persuade his shoppers to signal on along with his lawyer to sue Provider. The lawyer, Anthony Cuesta, hoped a court docket would seize Provider’s belongings to assist get better the buyers’ misplaced funds. However he rapidly realized there have been too many buyers and never sufficient fairness within the properties to fund the litigation. Now, lots of Welborn’s shoppers are ready for the FBI and DOJ to behave, whereas wealthier buyers are foreclosing on properties and making them ineligible for use for restitution. Welborn mentioned a few of his shoppers have been paid restitution via a DOJ-appointed actual property agent’s sale of Provider’s properties, however he declined to offer particulars.

Carver isn’t optimistic: “We’re not going to get a dime.”

Not less than one investor went after Welborn individually. Based on a Securities and Trade Fee disclosure, the declare was settled for $130,000. In his response to the SEC disclosure, Welborn denied breaching fiduciary responsibility to the consumer and mentioned he “resolved the declare to keep away from controversy.” Welborn advised ProPublica that $120,000 of the settlement got here from the sale of the home used as collateral for the household’s mortgage and he paid $10,000 for his or her legal professional charges.

Welborn mentioned he’s “devastated” by the lack of his shoppers’ cash. “However on daily basis I drag myself to work with God’s assist and spend most of my day serving to lenders with their very own private restitution battles,” he mentioned.

Some buyers mentioned they must return to work after having retired or are scrambling to seek out some strategy to change their misplaced earnings.

Carver needs he had paid extra consideration to pink flags, like paperwork errors. However the month-to-month checks have been so dependable, he didn’t hearken to his intestine. Or his spouse.

“Each time I added cash, my spouse would say, ‘Don’t do it,’” Carver mentioned. “My mom, too. She would push on my dad to not add any extra. However he preferred getting the month-to-month examine.”

Carver’s dad, Larry, believed it was the very best performing funding he had ever made. When the cash disappeared, Carver went to work making an attempt to recoup a few of it. Perhaps he might write it off on his taxes, he thought. He wished to get not less than one thing again for his dad. However Larry was in ailing well being, and in February, he died.

“My dad handed considering he misplaced all of his cash to this man,” Carver mentioned, including he hopes Provider “goes to jail for a really very long time.”

The investor who requested to not be named mentioned the loss was “a life-changing hit.” He had retired at 53, after sticking it out in a job he hated till his inventory choices vested. When he lastly stop, he put the cash into Provider’s enterprise and lived off of the month-to-month funds. He might have to return to work.

“He was an conceited son of a bitch,” the investor mentioned. “It was gone earlier than he advised anybody there was an issue. That’s the unforgivable piece. He squandered all of it away. And he needed to get backed right into a nook earlier than he admitted it was all gone.”

Byard Duncan contributed reporting.